What Is SIP? How It Works with Real Returns Example

What makes a small, steady investment turn into something substantial over time? Most people assume it requires either a large starting amount or perfectly timed decisions. In reality, it often comes down to consistency and patience, which is exactly what a Systematic Investment Plan, or SIP, is designed to encourage.

A SIP is a method of investing a fixed sum at regular intervals, typically every month, into a mutual fund. Instead of putting in a lump sum and worrying about when to enter the market, you spread your investment over time. This approach removes a lot of the emotional decision-making that tends to hurt long-term returns. You are not trying to outguess the market. You are participating in it, steadily.

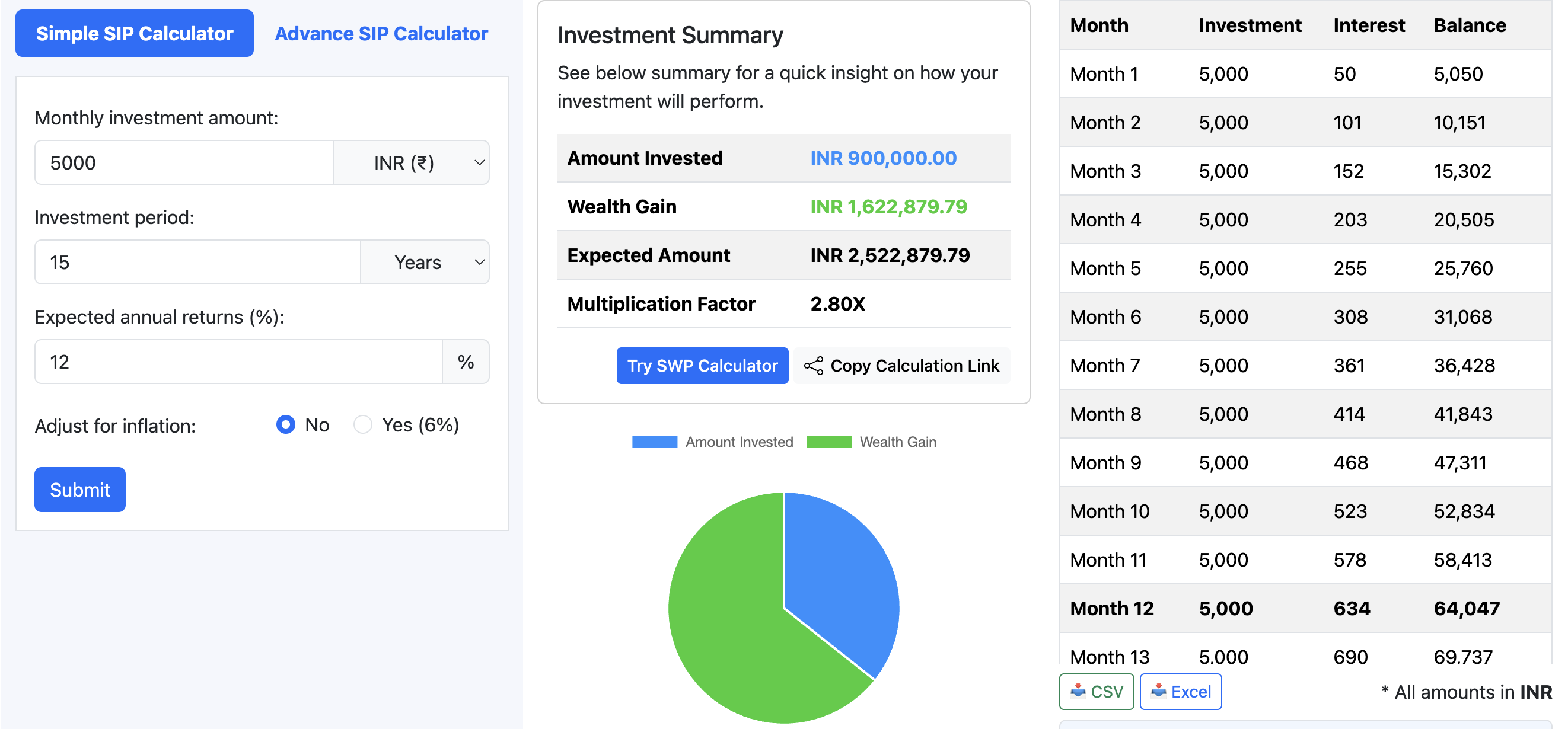

To understand how this plays out, consider a simple scenario. Suppose you invest ₹5,000 every month for 15 years, and the investment delivers an average annual return of 12 percent. Over those 15 years, your total contribution adds up to ₹9,00,000. If the returns hold close to that average, the investment could grow to around ₹25,00,000. That means the gains are almost twice the amount you originally invested.

At first glance, the numbers may seem surprising. After all, you are not putting in a huge amount each month. The key to this growth lies in compounding. When your investment earns returns, those returns are added back to your investment base. In the following periods, you start earning returns not just on your original contributions, but also on the accumulated gains.

In the early years, this effect is easy to overlook. The growth appears slow, and the difference between what you invested and what you see in your portfolio does not feel dramatic. This phase tests patience. Many investors lose interest or stop their SIPs here, thinking the effort is not worth it. But this is precisely the stage where consistency matters the most.

As time passes, the effect of compounding becomes more visible. The same rate of return starts generating larger absolute gains because it is applied to a bigger base. Around the later years of the investment period, the growth tends to accelerate. It is not because the market suddenly changed, but because your money had enough time to build momentum.

Another important aspect of SIPs is how they handle market fluctuations. Markets rarely move in a straight line. There are phases when prices rise steadily and others when they fall or remain flat. When you invest a fixed amount every month, you naturally buy more units when prices are lower and fewer when prices are higher. Over time, this averages out your purchase cost.

This process, often referred to as cost averaging, reduces the pressure of making perfect decisions. You do not need to worry about whether the market is at a peak or a dip. Your investment continues regardless of short-term movements. This can be especially helpful for those who find market timing stressful or confusing.

It is also worth noting that SIPs create a habit of disciplined investing. Because the investment happens automatically, it becomes part of your routine, much like a monthly expense. This reduces the temptation to skip investments during uncertain times or to divert the money elsewhere. Over long periods, this discipline often matters more than trying to chase higher returns.

That said, it is important to keep expectations realistic. The 12 percent return used in the example is not guaranteed. It is a reasonable assumption based on historical performance of equity-oriented mutual funds over long periods, but actual returns can vary. There will be years when returns are higher and others when they are lower, or even negative.

Market volatility is a natural part of investing. Economic changes, global events, interest rate movements, and investor sentiment all influence returns. A SIP does not eliminate these risks, but it helps manage how you experience them. By spreading your investments over time, you reduce the impact of entering the market at an unfavorable moment.

Another point to consider is the role of time. In the example, the investment period is 15 years. If you extend this period to 20 or 25 years, the final value can increase significantly, even if the monthly contribution remains the same. This is again due to compounding having more time to work.

Similarly, increasing the monthly investment slightly can make a noticeable difference. For instance, raising the contribution from ₹5,000 to ₹6,000 may not feel like a big change in the present, but over many years, it can lead to a substantially higher final amount. Small adjustments, when combined with time, tend to have a disproportionate impact.

Inflation is another factor that should not be ignored. While your investment may grow in absolute terms, the real value of that money depends on how prices change over time. Investing through SIPs in equity-oriented funds has historically helped in beating inflation over long periods, but this is not something that happens uniformly every year. It is a long-term outcome, not a short-term guarantee.

There is also the question of fund selection. Not all mutual funds perform the same way. Some may consistently deliver returns close to expectations, while others may underperform. Reviewing your investments periodically, without reacting to every short-term movement, is a sensible approach. The goal is not to keep switching funds frequently, but to ensure that your investments remain aligned with your objectives.

Taxes can also influence your final returns. Depending on the type of mutual fund and the holding period, capital gains tax may apply. While this does not negate the benefits of SIPs, it is something to factor in when estimating your net returns.

Given all these variables, relying on rough estimates alone may not give you a clear picture. This is where a SIP calculator becomes useful. By adjusting inputs such as monthly investment, expected return, and duration, you can see how different scenarios play out. It allows you to move beyond assumptions and understand the range of possible outcomes.

For example, you might want to see what happens if returns average closer to 10 percent instead of 12 percent, or if you extend your investment period by five more years. These small changes can shift the final numbers in meaningful ways. A calculator helps you visualize this without needing to do complex calculations yourself.

At its core, a SIP is not about quick gains or short-term wins. It is a method built around consistency, time, and the gradual accumulation of wealth. The simplicity of investing a fixed amount regularly often hides how powerful the approach can be when given enough time.

If there is one takeaway, it is that starting early and staying consistent tends to matter more than trying to optimize every detail. The exact returns will always be uncertain, but the process itself is designed to work with that uncertainty rather than against it.

Exploring your own numbers can make this clearer. Running a few scenarios through a SIP calculator can help you see how different choices shape your financial path, making the idea of long-term investing feel more concrete and less abstract.