Mutual Funds vs SIP: What's the Difference?

When people first start exploring investments, the terms "mutual funds" and "SIP" often get used almost interchangeably. It creates a bit of confusion. Are they the same thing? Is one better than the other? Or are they simply two sides of the same idea?

The truth is simpler than it seems. A mutual fund is the investment product. A SIP, or Systematic Investment Plan, is just a method of investing into that product. Once that distinction clicks, the rest becomes much easier to understand.

A mutual fund pools money from many investors and invests it in assets like stocks, bonds, or a mix of both. It is managed by professionals, which is one reason it appeals to people who do not want to pick individual stocks themselves. You can invest in a mutual fund in one go, often called a lump sum investment, or you can spread your investment over time using a SIP.

A SIP is not a separate investment. It is a disciplined approach where you invest a fixed amount at regular intervals, typically monthly. Instead of trying to time the market, you commit to consistency.

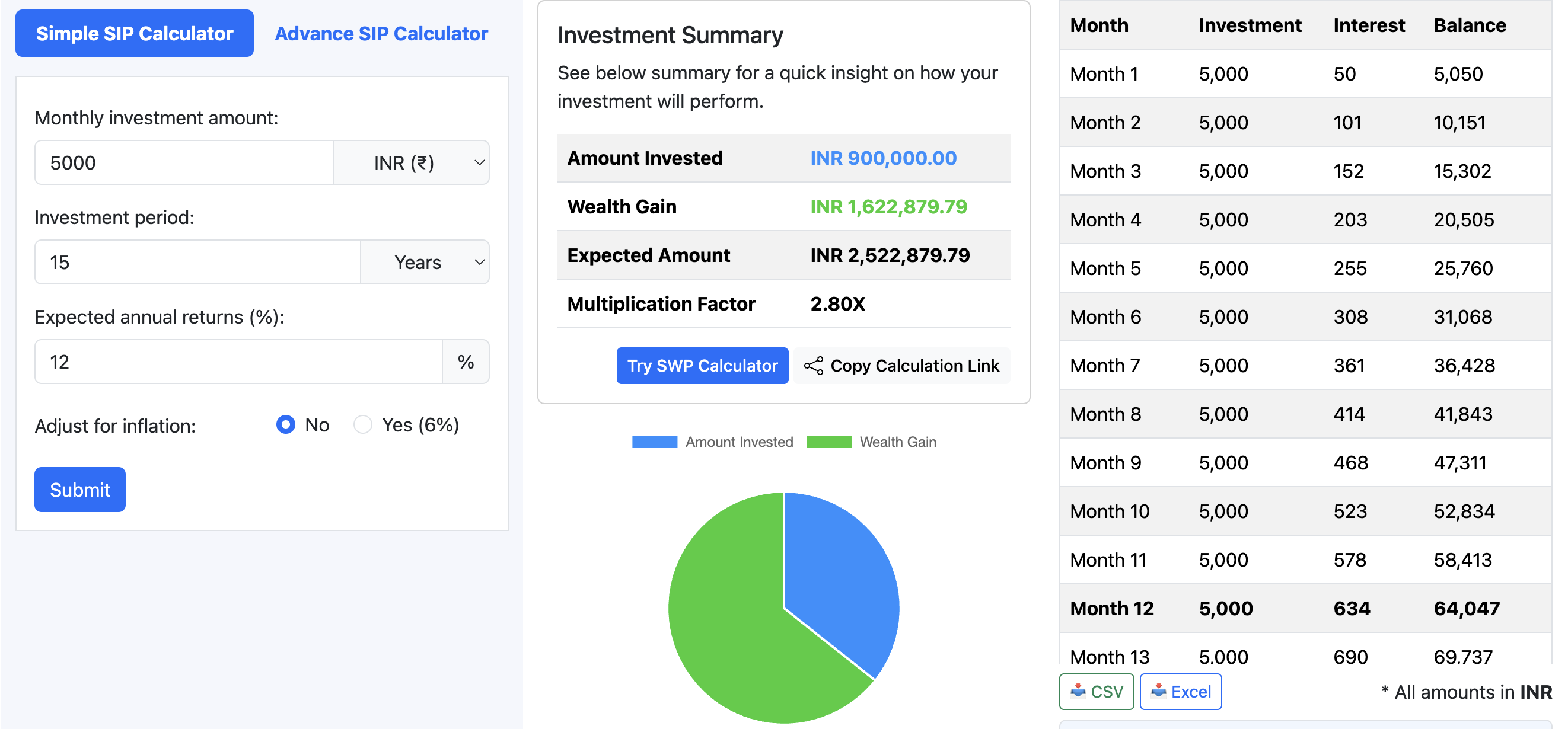

To make this more concrete, consider a simple scenario. Suppose you decide to invest ₹5,000 every month into a mutual fund through a SIP. You stay consistent for 15 years, and the investment earns an average annual return of 12 percent.

Over 15 years, you would invest ₹9,00,000 in total. That is just ₹5,000 multiplied by 180 months. But the outcome does not stop there. With compounding working in the background, the total value of your investment could grow to roughly ₹25.2 lakh.

That means your gains alone are about ₹16.2 lakh, which is significantly more than the money you put in. This is where the real appeal of SIP investing shows up. It is not about putting in large sums. It is about giving your money time and consistency.

The reason this works so effectively lies in compounding. Each month's investment starts earning returns. Over time, those returns begin to generate their own returns. The longer the time horizon, the more noticeable this effect becomes. Early contributions get the most time to grow, which is why starting sooner often matters more than investing larger amounts later.

There is another subtle advantage to SIPs that often goes unnoticed. Markets do not move in a straight line. Prices go up and down. When you invest through a SIP, you end up buying more units when prices are low and fewer when prices are high. This process, often called rupee cost averaging, smooths out the impact of market volatility. It removes the pressure of deciding the "right" time to invest.

That said, it is important to stay grounded. The 12 percent return used in the example is not guaranteed. Mutual funds, especially those linked to equities, are subject to market risks. Some years may deliver higher returns, while others may underperform or even show temporary losses. Over long periods, markets have historically trended upward, but there are no fixed outcomes.

This uncertainty is not a flaw. It is simply how market-linked investments behave. The role of a SIP is not to eliminate risk but to manage it better through discipline and time.

You might also wonder how changing the inputs affects the outcome. What if the investment period was 20 years instead of 15? What if the monthly amount increased gradually as income grows? Even small changes in these variables can lead to noticeably different results. That is where understanding your own numbers becomes important.

Rather than relying on generic examples, it helps to see how your specific plan might play out. A SIP calculator can give you that clarity in seconds. You can adjust the monthly amount, time horizon, and expected return to get a realistic estimate of where you might end up. It turns an abstract idea into something tangible. ▶ Try Our SIP Calculator Now

Coming back to the original question, the difference between mutual funds and SIP is not about choosing one over the other. You choose a mutual fund based on your goals and risk tolerance. Then you decide how to invest in it, either through a lump sum or a SIP.

For most people, SIPs offer a practical path. They align well with regular income, reduce the stress of timing the market, and quietly build wealth over time. Mutual funds provide the structure and professional management, while SIPs bring discipline and consistency.

When these two come together, they create a framework that is both simple and powerful. Not because it promises extraordinary returns, but because it makes steady investing easier to stick with. And in investing, consistency often matters more than intensity.