SIP vs Lump Sum Investment: Which Is Better for You?

SIP vs Lump Sum Investment: Which Is Better for You?

There is a moment almost every investor faces. You have money to invest, and the question is not whether to invest, but how. Should you put it all in at once, or spread it out over time?

This is where the choice between a Systematic Investment Plan and a lump sum investment starts to matter. Both approaches can work, but they behave very differently depending on timing, discipline, and market conditions.

To make this less abstract, it helps to walk through a simple, realistic scenario.

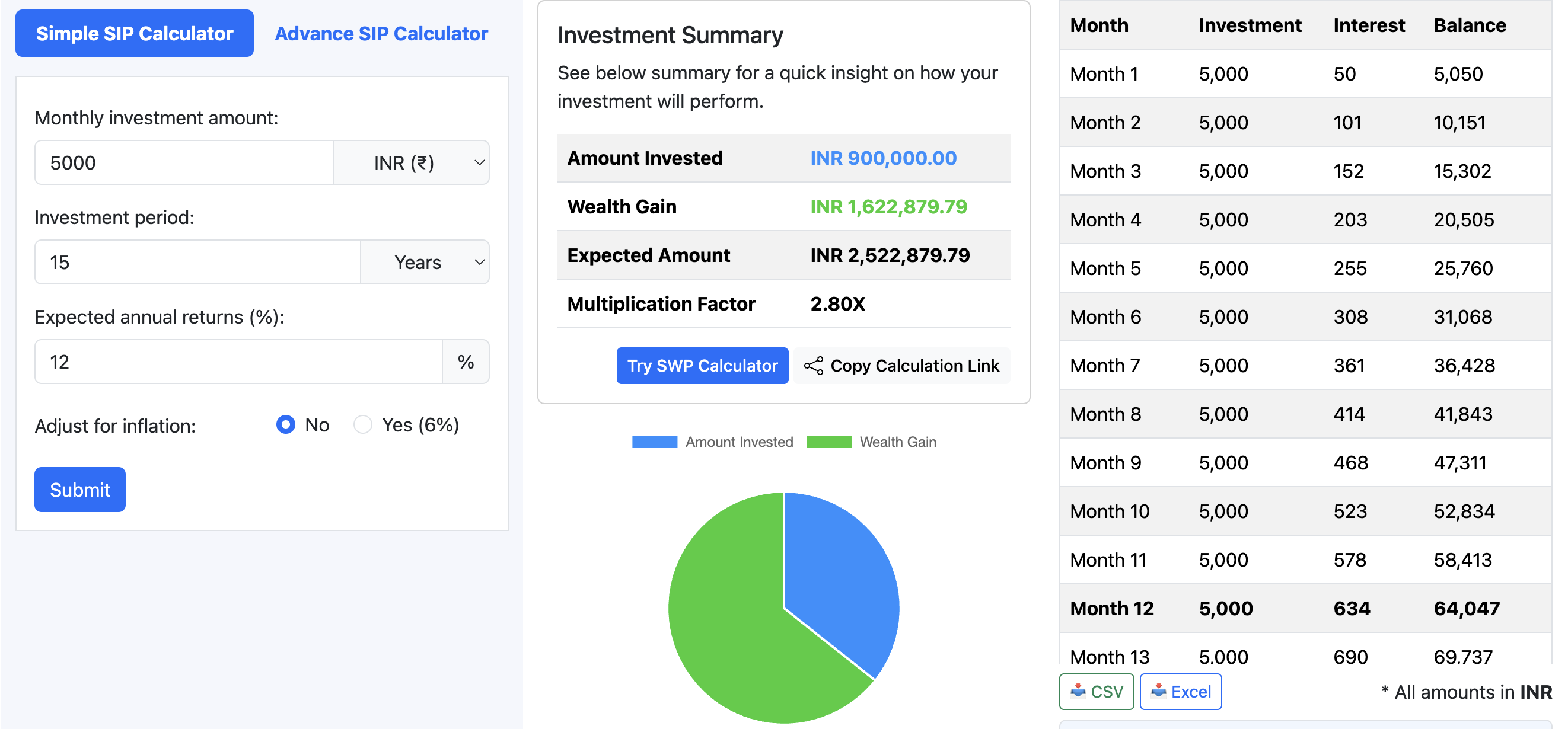

A Simple SIP Scenario

Consider someone who decides to invest ₹5,000 every month for 15 years. The investment goes into an equity mutual fund, and we assume an average annual return of 12 percent. This is a commonly used benchmark for long-term equity returns, though actual results can vary.

Over 15 years, the total amount invested would be ₹9,00,000.

Now, when you run the numbers using standard SIP calculations, the investment grows to approximately ₹25,20,000.

That means the gains alone are around ₹16,20,000.

At first glance, that jump can feel surprising. The invested amount is modest, but the final value is nearly three times higher. The gap between what you put in and what you end up with is where compounding quietly does its work.

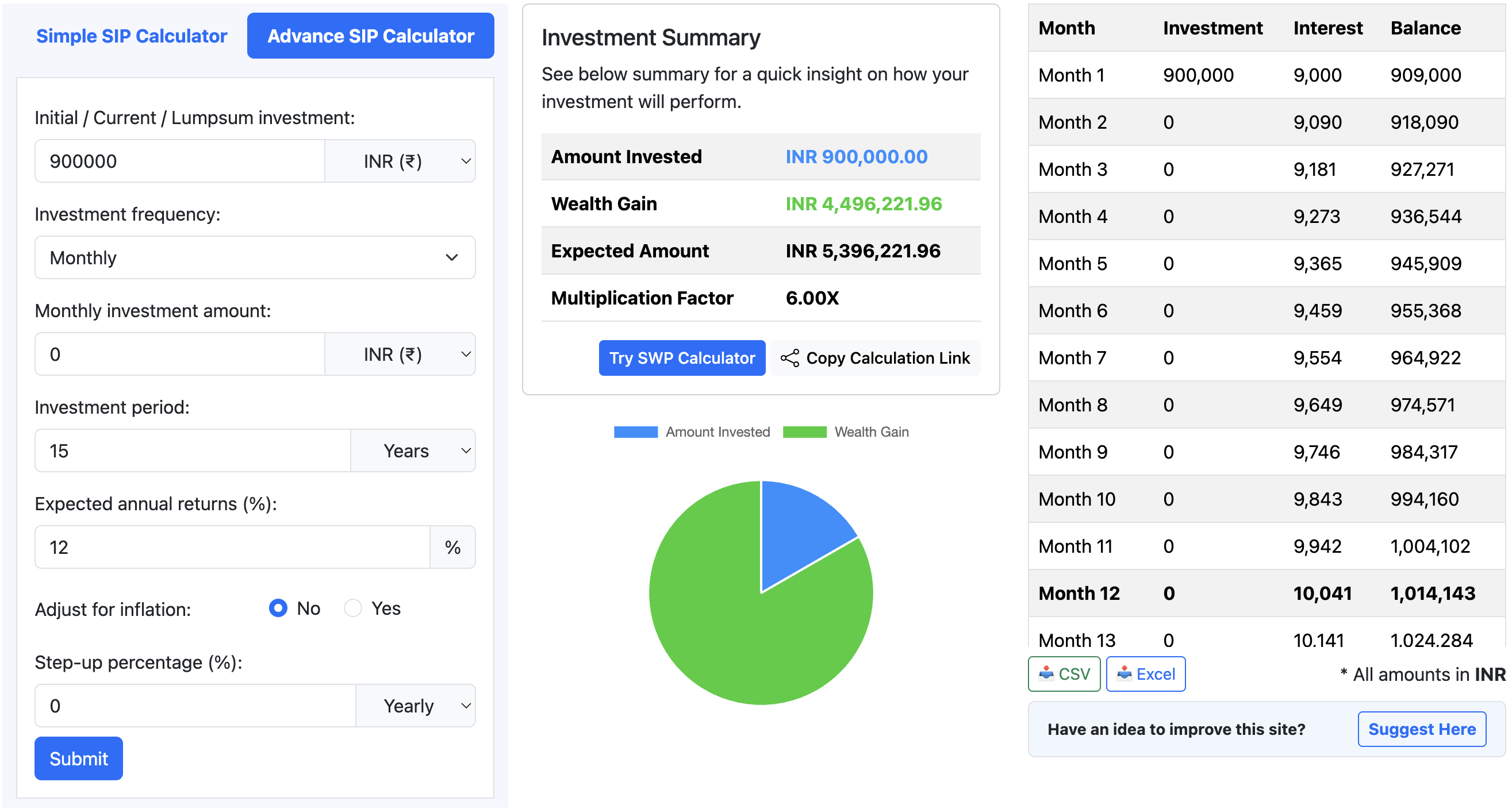

What Happens in a Lump Sum Case

Now consider a different situation. Instead of investing monthly, the same person had ₹9,00,000 available upfront and invested it in one go for 15 years at the same 12 percent annual return.

Over that period, the investment would grow to roughly ₹54,00,000.

That is significantly higher than the SIP outcome.

But this comparison needs context. The lump sum investor had access to the full amount from day one. The SIP investor built that investment gradually over time. These are not identical starting points.

The key takeaway is not that one is universally better, but that timing and cash flow play a big role in shaping outcomes.

Why the Difference Exists

The gap between SIP and lump sum outcomes comes down to how long the money stays invested.

In a lump sum investment, the entire amount gets the full 15 years to compound. Every rupee is working from the beginning.

With a SIP, each installment enters the market at a different time. The first few contributions get the full duration, but later ones have less time to grow. The last monthly contribution, for example, compounds for just one month.

This staggered investment pattern reduces the total compounding effect compared to a lump sum.

However, this is only one side of the story.

The Role of Market Timing

A lump sum investment benefits greatly when markets are low at the time of entry. But if the investment is made when markets are high, the initial years can be disappointing.

SIP works differently. Since investments are spread out, you end up buying at various price levels. When markets fall, your fixed monthly amount buys more units. When markets rise, it buys fewer. Over time, this averaging can reduce the impact of poor timing.

This feature makes SIP particularly useful for investors who are unsure about when to enter the market.

A Slight Variation in Perspective

Consider what happens if markets are volatile.

In a rising market, lump sum tends to outperform because early exposure captures the upward trend.

In a falling or sideways market, SIP often feels more comfortable because it smooths out entry points and reduces regret.

Neither method eliminates risk. They simply handle it differently.

For someone earning a monthly income, SIP aligns naturally with cash flow. For someone with a large surplus, lump sum becomes a practical option.

The Power of Consistency

One of the understated advantages of SIP is behavioral. Investing a fixed amount every month builds discipline. It removes the need to constantly decide when to invest.

This matters more than it seems. Many investors delay lump sum investments while waiting for the “right time,” which rarely arrives with certainty. Money often ends up sitting idle instead of growing.

SIP avoids this trap by turning investing into a routine rather than a decision.

A Reality Check on Returns

The 12 percent return used in this example is not guaranteed. Markets move in cycles. Some years may deliver strong gains, while others may see declines.

Over a long period, equity investments have historically generated returns in that range, but there are no fixed outcomes.

This uncertainty affects both SIP and lump sum strategies. The difference is that SIP spreads risk over time, while lump sum concentrates it at the beginning.

It is also worth noting that inflation plays a role. The real value of future returns depends on how inflation behaves over those years.

Which One Should You Choose?

The answer depends less on which method is “better” and more on your situation.

If you have a large amount available and are comfortable with market timing risk, lump sum investing can potentially deliver higher returns.

If your income is periodic, or you prefer a more gradual approach, SIP offers a structured and less timing-dependent path.

There is also a middle ground. Some investors choose to invest part of their money as a lump sum and the rest through SIP. This balances immediate market exposure with gradual averaging.

Why It Helps to Run Your Own Numbers

The example above uses one set of assumptions, but small changes can lead to different outcomes.

A higher return rate, a longer duration, or a larger monthly contribution can significantly change the final value. Similarly, shorter time horizons or lower returns will reduce the impact of compounding.

Rather than relying on generic examples, it is worth plugging in your own numbers. A SIP calculator makes this easy. You can adjust monthly contributions, expected returns, and duration to see how the investment might grow. ▶ Try Our SIP Calculator Now

This exercise often brings clarity. It turns abstract ideas into something more tangible.

Closing Thought

Both SIP and lump sum investing have their place. The difference lies in how and when your money enters the market.

For many people, the bigger challenge is not choosing between the two, but simply getting started and staying consistent. Once that habit is in place, the mechanics of compounding begin to take over.

If you are unsure where to begin, try mapping out a few scenarios using a SIP calculator. It can give you a clearer sense of what is achievable and help you make a more confident decision.